I just finished Carlota Perez’s Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages. First thought: not for everyone. It’s big picture tech cycle theorizing about economic history. Yet I found it first rate, and can see why it’s popular with some Silicon Valley investors. In particular Marc Andreessen cites Perez so often, I finally bought the book. It got me thinking. Our current tech cycle is well captured by Andreessen as software is eating the world. And software is highly prone to monopoly. Reading Perez, I found it hard to avoid the conclusion monopoly is eating the world. Attention must be paid.

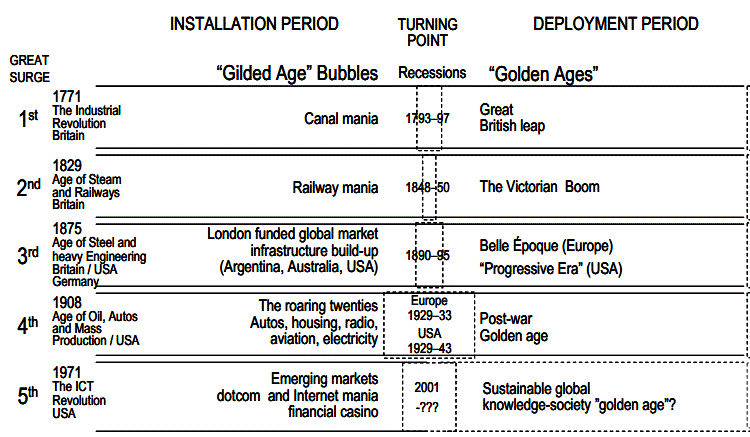

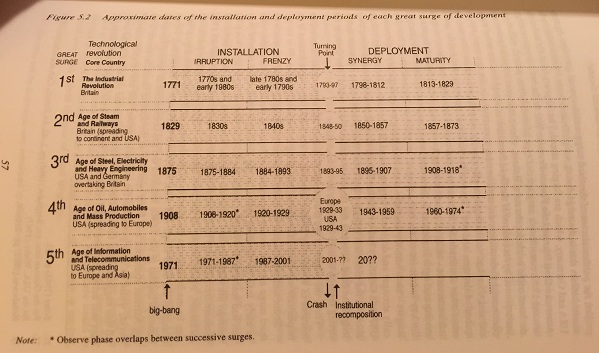

Perez is an advocate for what the economist Joseph Schumpeter dubbed Kondratiev waves, long boom and bust cycles driven by successive waves of technological innovation. Perez lists five technology surges:

- Industrial revolution 1771 to 1829 – textiles, wrought iron, canals, turnpikes

- Steam and railroads 1829 to 1873 – steam engines, iron/coal mining, railroads, telegraph

- Steel and electricity 1875 to 1918 – steal, chemical engineering, electrical equipment and networks, cables, telephone

- Oil, Autos, Mass production 1908 to 1974 – cars, cheap oil and petrochemicals, internal combustion engine, home appliances, refrigeration, roads, universal electricity, radio

- Information and Communication Technologies (ICT) 1971 to ? – microelectronics, computers, software, biotech, global digital telecommunications, internet, high speed physical transport

In chart form below, each wave has an installation period led by finance and free markets. This ends in a frenzied bubble with a financial crisis, creating a turning point that forces institutional reform. Then we get a deployment period where the wave spreads into the wider economy, led by production and the state. The deployment period starts as a golden age, but eventually the technology gets tapped out. Which creates an opening for the next cycle.

What I find most original (and for some reason neglected in reviews I’ve seen) with Perez’s version of Kondratiev waves is her thesis each wave is associated with a Thomas Kuhn paradigm shift. Note: jargon warning, she uses both paradigm and synergy extensively. For what it’s worth, I think she pulls this off. But mileage may vary. Perhaps the easiest way to illustrate her views on technology paradigms is by tracing historic shifts in the preferred metaphor for mind, as pulled from here. Stoics used fire as a metaphor for mind. By the industrial revolution it was clockwork. Age of steam was hydraulics. Then electricity. Then telegraph. Then electronics. Then computer hardware. And now of course the preferred metaphor for mind is software. What these metaphor shifts show is the technology of each age has such a profound impact on our world view, it alters how we perceive mind itself. Perez is saying the entire package of technology, beliefs, financials, and governance cohere together at the end of installation at the turning point, to form a cohesive whole for deployment. Each age is built upon the last, but incompatible with it. Paradigm shift. Let me pull a Marc Andreessen quote on adapting to our current software age: “People change, then forget that they changed, and act as though they always behaved a certain way and could never change again. Because of this, unexpected changes in human behavior are often dismissed as regressive rather than as potentially intelligent adaptations.”

The paradigm framework helps explain why innovation comes in waves. The underlying innovations may be discovered unpredictably, but they become bundled together into a single cohesive whole by human social psychology. Then get locked in place by market dynamics. Each age discovers the magic hammer they hope will solve all their problems: canals, railroads, and of course most recently internet/smartphone/software. And during deployment that hammer gets applied enthusiastically until it stops working. Perez ties the turning point of our current ICT/software age to the 2000 and 2008 crises, which means we’re now starting the deployment period. It’s time for existing companies to adopt. The deployment period for electricity was when we stopped having electricity companies, calling them companies. They all used electricity. Similarly we should expect the end of internet software companies as such, since all are adopting. Software has become water, and we are fish starting to swim.

Perez doesn’t spend much time on monopoly. But she does note it’s most likely to occur as a reaction to dwindling opportunities at the end of the deployment period, as the technology wave gets played out. She contrasts this with monopolies created in the frenzy phase at the end of installation, which form to curb price competition. Think crazy acquisitions in the dot com bubble in early 2000. Recall that Perez sees waves as technology bundles, so her focus on our current wave includes not just software, but also high speed transport, communications, biotech. And her book attempts to encompass all technology waves, so is less focused on the quirks of software monopoly. Perez does touch briefly on emphemerialization on page 225:

A growing portion of the economy, in terms of investment and trade, will be related to intangibles and will require appropriate instruments as well as conceptual creativity. How can knowledge capital be measured? Can it serve as collateral? What is the value of a product that is infinitely reproducible at almost zero cost? All those questions need to be solved in practice for the system to flow.

In contrast to Perez, I see software as the single and clearly dominate technology of this tech cycle. One that can absorb and become a front end to all the others. Obligatory Andreessen cite:

http://twitter.com/pmarca/status/657777105019604992

But what of Moore’s Law? As it unlocks more and more possibilities, such as machine learning, driverless cars, internet of things, and talking computers, this wave may turn into an unending, or at least greatly extended, installation period frenzy. Let’s return to Perez’s paradigm framework, especially as applied to social psychology. We have to ask whether the software age norms we have today can withstand a few more decades of Moore’s Law. Those norms are distilled to their essence in Venkatesh Rao’s Breaking Smart essays. Small elite teams with a hacker ethos. Incremental but compounding change. Trial and test. Agile methodologies. Lean. Iteration. Iteration. Iteration. Well worth reading. (I can also recommend Rao’s ribbonfarm site). Once put in those terms, it’s clear the hacker paradigm can not just withstand the exponential rocket of Moore’s Law, it was born of it. It’s a paradigm now so perfectly adapted to Moore’s Law it has become parasitic. Continuing exponential growth in computational power makes it stronger. Any slowing will weaken it, perhaps to fatal effect.

This dynamic makes the current software driven technology cycle somewhat unique. During the deployment period we are in right now, the paradigm is understood and existing companies can uptake the technology using their own production capital. Financial capital (think Venture Capital) should be sidelined, or put to work creating the next wave. Instead, and to be clear this is just my own take on Perez, what’s going on is Moore’s Law is allowing disruptive opportunities to exist well beyond the traditional Perez turning point, into the deployment period itself. If this is true, Venture Capitalists may well remain happy a bit longer. Though I suspect what it takes to be a good VC during installation frenzy is quite different from what it takes during a deployment build out. It’s also worth noting the hacker ethos, which assumes a permanent state of radical change, has a natural blind spot to the dangers of monopoly. A word which of course never appears on the Breaking Smart site.

Now some caveats. Economists have very mixed views on Kondratiev waves. Though Perez is (at least to me) suitably cautious. I’m also skipping a lot from her book, especially her discussion of capital, to focus on software monopoly. If you want to dig deeper, I recommend Jerry Neumann’s recent Perez explainer post. Or get the book.

Every tech cycle has its great institutional challenge. Software monopoly is ours.

As I write this, I searched Google for “software is eating the world” and got back 157k results. A search for “monopoly is eating the world” returned 0. Though to be fair that number will go to 1 after I post. It’s almost as if investors have an unspoken agreement to downplay the rise of software monopoly. Of course Warren Buffett has always said investors should seek companies with an economic moat, protections from competition. But the terminology is changing with the times. Less moat. More monopoly. As the wonderfully outspoken Peter Thiel puts it: “Competition is for losers.” Here’s Sam Altman on what he looks for in startups: “We also ask how the company will one day be a monopoly. There are a lot of different terms for this, but we use Peter Thiel’s. Obviously, we don’t want your company to behave in an unethical way against competitors. Instead, we’re looking for businesses that get more powerful with scale and that are difficult to copy.”

The economic drivers of natural monopoly are high fixed costs, economies of scale, network effects, and nonrivalry (zero marginal cost to produce copies). Software has all this in spades. Winner take all. One nuance to software’s zero marginal cost structure is it can cut both ways. It can allow entrenched players to drive out competitors and reap profits. Or when barriers to entry remain low or software gets bundled with other products, it can drive prices to zero. Examples being open source software, consumer operating systems, and most apps in the app store. But even in those cases, a winner take all dynamic pertains. Niche apps are somewhat protected due to market size. But the more important to society and the larger the scale, the more monopoly matters. The internet has been adding scale while removing friction and disintermediating middlemen. It used to be consumers had to buy software on disks from stores. Now apps seamlessly update on phones. Businesses formerly had massive costs trying to get enterprise software to work on-premise. In fact it’s always been a dirty secret of enterprise software deployments that a large fraction failed. With cloud and SaaS business models, that friction is removed. In fact since businesses buy through a centralized and highly complex procurement process, they tend towards incumbents and monopoly even more than consumers. Longer term, expect friction to be removed from banking as well, as bitcoin and blockchains remove friction from ledgers, payments and contracts. Every step forward in internet technical progress pushes software economics closer to the platonic ideal of natural monopoly.

Monopoly also has a rather devious lifecycle. Getting to monopoly scale means winning customers the hard way and beating ferocious competitors. So early on, monopolies are often beloved. And deservedly so! Uber is great. But then the brutal success culture that makes them win, makes them terrible monopolists. Dominance removes incentives for improvement, increases incentives for leveraging monopoly into adjacent markets, and increases incentives for regulatory capture (getting in bed with government regulators). Lawsuits can then drive the monopoly life cycle to its logical conclusion. Either a damaged company drifting towards slow decline (think IBM, which shows there’s a great deal of ruin in once great companies), or an industry so dependent on regulatory capture it can’t function without it (think Amtrak railroads or New York City taxis). I’m old enough to remember how in small towns like the one I grew up in, we were desperate to get cable TV. Truth: “I want my MTV” was once a thing. Yet now, decades later, searing hate for Comcast Cable regularly sets fire to my twitter feed. IBM was also once loved, then sued, then hated. Microsoft’s fierce competitive brilliance made it succeed. Then drove it to wield its monopoly power to put Netscape out of business. When the lawsuits came, Microsoft was blindsided by the fierce hate they had provoked. Like many great companies, Microsoft’s self image and culture formed early, remaining nearly impervious to later events. This excerpt from Charles Arthur’s Digital Wars book captures it well, and is more relevent than ever.

One terminology point. I’m using the term monopoly informally to mean monopoly power. For example, Google is not a monopoly. There are alternate search engines. But Google does exert dominant market power in search and web advertising, which they can leverage to pry open other markets. Technically this is an oligopoly where the dominant player has massive market power. An alternate title to this piece is “software has a strong innate tendency towards skewed oligopoly with a single dominant player, which Nobel winning prize economist Jean Tirole has shown leads to information asymmetry between regulator and regulated, and game theory proves can, if unchecked, result in super bad things.” But I think “monopoly is eating the world” works better.

Monopoly: past, present, future. Software companies at scale must have an antitrust strategy.

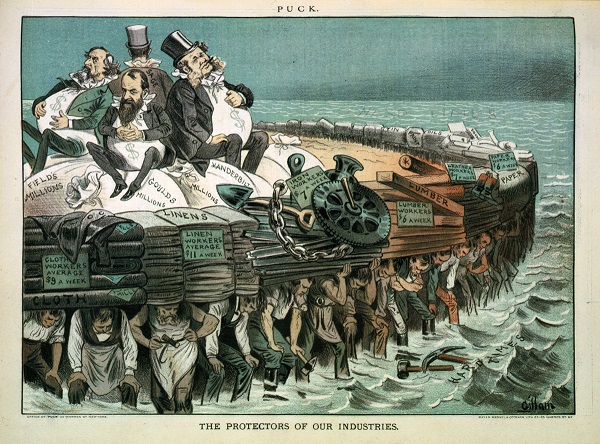

Monopoly is not new. Above is a Puck cartoon with the railroad tycoon Cornelius Vanderbilt seated on the far right. Railroads were the poster child for monopoly during Perez’s second tech cycle, which she tracks as 1829 to 1873. What’s notable is the full institutional response to railroad monopoly did not occur until 1890, during the turning point of the third tech cycle. By then problems with monopoly trusts (cross company ownership, which enabled price collusion) were so severe the Sherman Antitrust Act passed. This and the subsequent Clayton Act set the model for modern competition law globally. As the Microsoft case shows, that law can be used against software monopolies. But the history of railroads show us there may be a great delay in adjusting existing laws to match the times. You go to battle with the army you have.

What are possible responses to monopoly? Below is my list. Following Perez, these responses are more than just government. Corporate structure, norms, best practices are all part of the new paradigm.

Responses to Software Monopoly:

- Lawsuit to cripple. The IBM and Microsoft monopoly lawsuits damaged them enough to leave space for the next wave, but didn’t really change their existing business. The primary pain was not about money, but damage to reputation for future hiring, morale within the company, and wariness to any type of aggressive expansion outside their core (constant second guessing on whether proposed actions could be construed as destroying the next Netscape).

- Lawsuit to break up. The 1911 break up of Standard Oil is the canonical example. Another being the 1982 break up of AT&T into the so-called Baby Bells. And of course breaking up Microsoft was the original judgement, splitting Windows from everything else. Though that was later reversed.

- Prop up one weak competitor. During its heyday, Intel kept AMD alive deliberately so it could have a competitor and avoid antitrust. In 1997, Microsoft did the same with Apple. Of course both Intel and Microsoft later got sued anyway, but their actions mitigated their problems at the time.

- Only sell to premium customers. This is the Apple model. And it protects them quite well from antitrust. In some sense it’s similar to #3 above, as the company focuses only on a limited segment of the market, leaving other customers alone. But the internal corporate cultural dynamics of premium are quite distinct. Of course Apple bundles their zero marginal cost software with their hardware. I suspect the premium approach works best (or perhaps only) with a bundling strategy of some sort, with the software itself priced at 0.

- National champions. In this model, each country or economic region gets its own monopoly, which competes internationally. Think Airbus versus Boeing. With Tencent, Alibaba, Baidu, Netease, etc., we can just call this the China model. It’s less clear whether it will catch on in Europe or other parts of Asia. I think it could, but will be difficult to adopt this late in the tech cycle. Note this approach is highly prone to crony capitalism, so may look good early on if industrial policy is set wisely, but later stagnate as incumbents got frozen in place by government symbiosis.

- Monopoly is fine. Competition is for losers! This is Peter Thiel’s solution. Quote: “If the tendency of monopoly businesses was to hold back progress, they would be dangerous, and we’d be right to oppose them. But the history of progress is a history of better monopoly businesses replacing incumbents.” And “So why are economists obsessed with competition as an ideal state? It is a relic of history.” I just love a good Peter Thiel quote! What’s great is there’s some deep truth here. IBM really was overtaken by Microsoft who was later overtaken by Apple/Google in mobile. Monopoly displaced monopoly. And note that the faster the pace of change, the better this works. It perfectly represents the hacker world view. But I think the consensus reading is #1 above played a big part in what happened as well. Antitrust lawsuits crippled IBM and Microsoft enough to allow space for the next wave.

- Monopolies competing along asymmetric axes. This is two monopolies competing, but not head to head like traditional oligopolies. Not Pepsi against Coke. Instead it’s monopolies challenging each other along the edges using asymmetric business models. Think Apple selling proprietary mobile phones against Google selling ads and giving away open source Android. Or Amazon as web retailer selling movies against Apple. Facebook’s social network selling ads against Google’s web search ad model. Microsoft in enterprise computing attempting to push into consumer against Apple. This is a real thing, and far more common now than in previous tech cycles since all these companies are software centric and more technically capable of going after one another.

- Regulated utility. Water, electricity, sewage, garbage, cable tv are all regulated utilities. Of all the monopoly responses, this is the default. It works. But it’s not pretty. One perverse dynamic of regulating companies as utilities is they become even more entrenched through regulatory capture. The more the European Union binds Google with rules for privacy and rules for how it can compete, the harder it becomes for a new entrant to displace them. And it’s politically hard to get regulations right, one annoying example being how cable broadband regulations in the US don’t use the superior local loop unbundling approach used by many other countries.

- Open Source. The importance of the open source movement for containing software monopoly can’t be overstated. Of all the monopoly responses listed here, open source is the only one born native to the software age. Open source removes the risk of software monopoly by leveraging the very thing that makes it so dangerous: zero marginal cost. The internet as we know it today is a triumph of this movement. When Red Hat said they could build a business on top of free software in 1993, it was not clear it would work. Today they have a nearly $15 billion dollar market cap. Automattic/Wordpress, Cloudera, and of course Google Android all come to mind. Ben Thompson has a very good recent piece on why bundling open source with some other angle of differentiation is such a powerful competitive approach. He uses Google’s recent open sourcing of their machine learning system TensorFlow as his example. What I want to add here is open source is also a very very sharp strategic move to avoid antitrust lawsuits down the road.

Back to our Sam Altman question, asking “how the company will one day be a monopoly.” That’s exactly right for starupts. But for those select few startups who achieve their dream of scaling to massive size and power, a follow up question must be asked. What is their preferred response to antitrust, given the choices above? Software companies at scale must know their strategic answer to that question. I suspect most don’t want to be a regulated utility. But that’s pretty much the default answer if you don’t have a plan. In fact a few years ago I wrote about how Google was on the path first towards a conglomerate (a step now complete), and then towards regulated utility (a step now looming in web search). See here. If a company waits until monopoly antitrust becomes a critical problem, it’s probably too late to adjust their approach. It may be too late for Google search, but perhaps Google machine learning will turn out different.

Perez technology cycles run on a clock measured in decades. So no need to panic. And the early part of the monopoly lifecycle is actually pretty great for everyone. It’s just later on when it becomes a problem. What is also now clear is the great temptation of our age of natural monopoly is regulatory capture and crony capitalism. We should not be surprised if we soon see an updated Piketty 2.0 message by progressives on inequality, singling out software robber barons for reform. In fact there’s a reasonable case to be made that the slowdown at the end of each Kondratiev waves is not driven by technology exhaustion so much as by regulatory capture for the economy as a whole. And only disruptive technology and business models outside the existing regulatory framework are able to punch through that stasis. Taxis might have considered inventing Uber, but capture made executing on it simply impossible.

As we continue into the deployment period, software will become the front end to the largest sectors of the economy: transportation (Uber, self driving trucks and cars, drones), health care (AI diagnosing patients, electronic health records, constant health monitoring), finance and banking (bitcoin, blockchain, contracts), retail (Amazon), education (MOOCs, self teaching), etc. These are the sectors where the temptation of crony capitalism will be greatest. Today our economy is dominated by oligopoly. And we have the institutions and governance to match. We know how to muddle through with oligopoly. It’s flawed but comfortable. As software is eating the world, we need to adjust those institutions. And not be shocked to find monopoly is eating the world too.

__________________________________________________

Appendix – more links on this topic

- Andresseen’s classic Why Software Is Eating The World

- Jerry Neumann’s excellent explainer on Carlota Perez The Deployment Age

- One thing I searched for was economic data to support the thesis above, which predicts market consolidation as software takes over a sector. For example, consolidation when smartwatches take over from existing ones. And….I searched a bit, but didn’t find anything definitive. Though likely it exists. Closest I got was this article Monopoly and Competition in Twenty-First Century Capitalism

- The Economist on internet companies and monopoly, no Perez and a bit more narrow, but quite good on same topic Everybody wants to rule the world

- Ben Thompson on open source as competitive approach Tensorflow and Monetizing Intellectual Property

- My two earlier pieces on software monopoly. What’s new in the post above is the Perez framing, which I think makes it better than the old ones. The first about Google, the second framed by disruption and monopoly life cycles.

{kind=link}

Interesting. There’s a related question I’ve had, as you’re an econ shark maybe you have thoughts. Is it better* for antitrust to focus on protecting companies from a monopolist, so that more companies can thrive in an industry and thus create more jobs (as well as potentially more innovation)? Or is it better for antitrust to focus on protecting a monopolist such that they can drive lower prices through economies of scale (assuming they don’t then raise prices through monopoly rents), thus saving the average consumer a few bucks?

Let’s leave Amazon aside as the obvious recent example, let’s take Uber. Is it “better” if Uber becomes a monopoly and thus a ride costs $9 instead of $10 if it were a sub-monopoly scale, so that millions of consumers each save a buck per ride? Or is it better if Lyft, Hailo, Didi Kuaidi et al survive such that 10 companies in aggregate offer 5,000 more jobs at $50k/yr. salary?

Maybe not a great example but I think you get my question. Current courts seem to want to protect consumers at the expense of competition. Was that always the case, and is that accepted economic theory or does that view shift with the winds?

* for some definition of better, e.g. overall impact on a country’s economy

This is a hard question, not sure of answer. But here’s my thoughts.

First, as you likely know, we have a test case for this. The US protects consumers, while the European version of antitrust fosters competition. Which works better? In practice the European version tends to have more regulatory capture as the state decides who wins. And the US if more lenient. So in that sense I suspect US works better since it’s far more open to new entrants, which is the long run is what really matters. But the downside of US approach is that when they do regulate, they do it badly. The classic example I mentioned above is broadband in the US being awful, and in fact far less competitive than elsewhere.

The ideal case partitions the regulated utility into the smallest box possible. In our example with local loop unbundling is the way to go with broadband since it puts the infrastructure into the different box than the broadband providers.

http://www.motherjones.com/kevin-drum/2014/02/want-better-broadband-unbundle-local-loop

So I’m a mild yes for US approach. But really what we need is far better regulation, which is hard in any regime. It’s good governance.

Looks like others are starting to see the notion that consumer surplus is not a broad enough lens in determining antitrust issues: http://www.yalelawjournal.org/article/amazons-antitrust-paradox

I’ve written quite a lot about Perez (see my blog: https://thenextwavefutures.wordpress.com/?s=perez), and your list of delaing with monopoly misses one important market-driven effect which is in her model. In the last quarter of the surge (which is just about where we are with the ICT surge) you see high levels of market penetration and high levels of commoditisation. In other words, there are not new customers to be found (or only marginal low value ones) and the margins on what you make and sell are also falling. So it becomes harder to justify investment in new products and services. Actually, we’re seeing quite a lot of this in the ICT sector already.

Second, in the final quaretr you get user and regulatory push-back against the dominance of the surge’s products in the market: if you think about the auto surge, it was in the last phase (60s) that we started to see (for example) parking restrictions, limits on drink driving, compulsory safety measures like seat belts, and campaign groups questioning the near for public support for the technology and its infrastructure (think: Janes Jacobs vs Robert Moses in NY). All of this is effectively about limiting the external costs of the technology and its users. Again, we’re seeing this, both at market and regulatory level with ICT.

But the dominant assumption that the technology is the future – in the minds of advocates, politicians, etc – remains almost until (or even after) the surge is over. This is partly because the economic and social effects of the next surge are weak in the first quarter of the deployment phase. Again, thinking about ICT, there were lot of prefigurative technologies (punch cards etc) before the microprocessor in 1971, but even in the second part of the deployment phase – say ’89 to ’02 – market penetration was low. Even at the time of the dotcom crash in the leading markets (US, UK) penetration of internet use was 25% or less, although PC penetration was higher.

Thanks for your comments. I read a few of your posts as well. Good stuff! You have written about this quite well.

Let me restate your points to make sure I get them, then respond. You say:

1. later in deployment (past synergy towards maturity), profits dwindle, reducing investment.

2. Also at that time, regulatory control asserts itself more strongly

3. People retain faith in the wave even past when they should.

I think this is compatible with my post, although you seem to be saying point #1 implies less incentive towards monopoly. Now, I had saved some notes from when I wrote this post. A quote I didn’t add to my original post above (it was already too long) is from p. 82 of Perez’ book:

“One of the early solutions that the most powerful firms find to confront the signs of exhaustion is increasing market control. This is achieved by various means: through mergers, as were the railroad ‘amalgamations’ of the 1860s in Britain, by squeezing out of the market or buying up smaller competitors to create closed oligopolies or by acquiring firms in other sectors to build diversified giants, as with the conglomerate wave in the USA in the l960s. This type of drive for monopoly power is a response to dwindling market growth. It should be distinguished from the concentration trends that will happen later, towards the end of the frenzy phase of the next paradigm. In that period, markets will be growing strongly in ferocious competition, so mergers and acquisitions seek, among other things, to reduce both the number of competitors and the intensity of price competition. By contrast, in the maturity phase being discussed now, economies of scale are sought to capture a larger share of saturated and diminishing markets.”

I believe what Perez is saying is that as profits get squeezed toward the end of the cycle, consolidation occurs to capture oligopolistic profits. The second part of the quote says monopoly can also happen during frenzy, just before the turning point. But that this class of monopoly is of a different sort. It’s a market grab during the boom. To get back to your point #1, I believe she is saying (and I agree) that dwindling profits in fact drive companies towards monopoly. Not away from it.

I do agree your point #2 is starting to happen, for example Google antitrust in Europe, as mentioned in my post. Agree this will help control monopolistic tendencies.

I’m not sure #3 relates to monopoly per se. But totally agree.

Thanks for taking the time posting a good comment. I also enjoyed your blog.