It is hard to overstate the influence of Bentley University’s Scott Sumner on monetary policy since he started blogging at The Money Illusion in Feb 2009. Sumner has pushed economists close to acknowledging that the Fed is to blame for one of the largest economic policy disasters since the Great Depression.

To understand, it helps to break out macroeconomists into schools of thought:

- New Keynesians – This includes most of the progressive/liberal economists. In the econ blog world this would be people like Paul Krugman, Matthew Yglesias and Brad Delong, plus also people like David Romer, Joseph Stiglitz and Nouriel Roubini. To simplify, their solution to mass unemployment is either fiscal stimulus (tax cuts or increased government spending) or monetary policy (in particular lowering interest rates).

- New classical macroeconomics – This includes old school rationalist expectations economists like Robert Lucas plus finance people like Eugene Fama. They are generally skeptical of either fiscal stimulus or monetary policy. Basically there’s not much you can do in a downturn except wait it out. Many conservatives hold or are influenced by this view.

- Market Monetarists – The term itself was only coined in 2011 in response to people coalescing around Scott Sumner’s views from his blog. Market Monetarists focus on managing the money supply, in particular wanting to boost it to help the economy recover. Market monetarists derive from the Milton Friedman school, but it’s important to note that’s true of the new classical economists as well. Historically both are associated with a more conservative view. In one case the Fed should be do little (new classical), and in the other act only within well defined rules (monetarists). Right now conservatives are unfortunately more in the do nothing new classical camp, which Friedman undoubtedly would disagree with. So Monetarists are a bit in the wilderness from a political backing point of view.

The problem with New Keynesians is when interest rates are close to zero, as they’ve been since the 2008 downturn, all that’s left is fiscal stimulus. Interest rates can’t go lower. And if you can’t pass politically tough fiscal measures like tax cuts or increased government spending, there’s nothing left you know how to do. This is Japan’s lost decade and what the US is doing now.

Scott Sumner had an excellent recent post entitled “Where did Obama get the crazy idea that fiscal stimulus was the only option?” What’s shocking is that the New Keynesians clearly stated that fiscal stimulus was the only option during the 2008-2009 financial crisis. In his post, Sumner quotes several prominent people like Paul Krugman from that time period, but really it was the larger view of economists in general including Obama’s economics team. In fact Sumner got into blogging for precisely this reason, because he was surprised to see so many economists who seemed not to have learned the lessons from the Great Depression.

Now the New Classical Macro school thinks there’s not much you can do in a downturn anyway. So you can’t expect policy recommendations from this school so much as critiques that you can do anything at all.

Finally, the Market Monetarist school believes in bumping up the money supply through a variety of tools within the Fed’s power, such as quantitative easing. In fact they advocate targeting the Nominal GDP by the Fed as a rule, rather than the dual unemployment/inflation mandate the Fed currently uses. This is called NGDP targeting. At the zero bound (interest rates of zero), there are still tools such as the Fed buying bonds that can inflate the economy. What this does is allow the Fed to solve the unemployment problem even at the zero interest bound. To see what this means, first recall that “real” means inflation adjusted to an economist. And “nominal” means not inflation adjusted, just the raw dollar number. So to target NGDP, all the Fed needs to do is make sure that the national Gross Domestic Product in raw dollar value goes up along a straight line over time. You don’t care if the real (inflation adjusted) economy is growing or not, you just add to the money supply as needed during a downturn to make up the difference. What’s brilliant about this is it’s automatically counter cyclical, it provides clear expectations to businesses on what the future should be like, and it works even at zero bound.

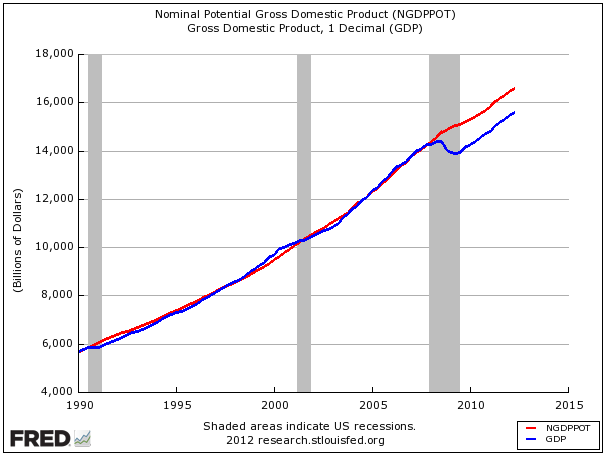

Over the past 3 years, Sumner and the Monetarist school have slowly won over the New Keynesians to agree that NGDP targeting is the way to go. Although many Keynesians still prefer interest rate lowering or fiscal policy, most are now on board with NGDP targeting in the current situation with high unemployment and zero interest rates. So for instance we see this join the bandwagon article from Oct 2011 where Krugman, Yglesias and others have reversed their older views. And just this week Michael Woodford, “widely regarded as the greatest monetary economist of his generation” has published an 87 page paper favoring NGDP targeting as well. Woodward says to target NGDP you tell the markets that “We are going to keep rates low until the blue line comes back and touches the red line.” The blue line below is nominal (not inflation adjusted) GDP, and the red line is what nominal GDP would be assuming full employment. The quote and chart below are from this article, which has a good explanation of the paper.

The implications of this shift in economic thought are enormous. What it says is the stickiness of high unemployment four years after the financial crisis is the Fed’s fault. By NGDP targeting and better Fed policy, the recovery would have been quicker, and in particular millions of people who are currently out of work would have jobs today. It’s a shame neither political party is willing to talk about this more. Millions of Americans as suffering with excessive unemployment needlessly. On the liberal side, discussing this topic would mean Obama would have to admit Fed Chairman Ben Bernanke failed, or more accurately could have done a far better job. Which is especially tragic since Bernanke is an expert on the Great Depression, as Sumner is, and Bernanke is duplicating some of the mistakes he said we should never make again. And Obama failed in appointing better Fed officials. On the conservative side, it would mean accepting that government action has a place. In particular it means the Fed needs to take action, which conservatives especially hate since they are currently more enthralled with the new classical macro school rather than Friedman and the monetarists. In the end, neither side wants to blame themselves, so the Fed’s role in mass unemployment is off the table during the current election cycle. And the public continues to incorrectly believe that the main cause for continuing high unemployment is the financial crisis of 2008, rather than Fed mismanagement of the money supply since then. Both parties are avoiding the most critical public policy failure of our time.

On the plus side, Sumner has been saying for years there’s no conspiracy to avoid fixing high unemployment. After all, how could we expect the Fed do anything other than what most economists felt was the consensus course of action? So by slowly swaying the New Keynesians over to his side, Sumner has moved NGDP targeting closer to the mainstream, which in the end is what’s needed change Fed policy. This can happen regardless of any election cycle. Hopefully the Fed will bow to the relatively new consensus soon, moving away from piecemeal quantitative easing to full blown NGDP targeting. If not, then we’ll lose a decade as interest rates slowly crawl past the zero bound, where old school Keynesian techniques come into play. No matter how it plays out, don’t expect anyone to find fault with themselves. But to the extent Fed policy improves, lifting millions of people out of unemployment, let’s give credit to the total awesomeness of economist Scott Sumner.

PS Update: Posted this on Sep 9, and coincidentally Matthew Yglesias made the same point with a post called “The Scott Sumner Rally” with the very same picture on Sep 13.

2 comments